In Brief

Senegal is the presource curse in real time. Between 2014 and 2024 — the decade spanning discovery and first production — the country accumulated an extra $7 billion in debt that its previous government systematically concealed from the IMF, its parliament, and its citizens. Public debt rose from around 45% of GDP to over 100%. When production finally began in June 2024, Senegal entered the revenue phase carrying the full weight of its presource borrowing.

Growth Outcome vs. Counterfactual

The chart below shows actual total GDP (navy) against the IMF WEO rolling 1-year-ahead forecast chain from the discovery year (amber dashed). Both series use IMF WEO data, indexed to the discovery year = 100. Shading highlights the direction of the expectations gap: amber where the forecast exceeds actual, navy where actual exceeds the forecast.

Anatomy of a Lost Decade

Total GDP trajectories for resource-discovering countries — actual outcomes vs. IMF forecasts at time of discovery. Index: discovery year = 100.

Source: IMF World Economic Outlook vintage forecasts (actual growth and 1-year-ahead forecast chains). Amber shading: forecast exceeds actual (over-forecast). Navy shading: actual exceeds forecast. Both series indexed to discovery year = 100. 9 countries covering SSA hydrocarbon and copper discoveries, and Guyana.

Borrowing Against Expectations

The chart below shows how central government debt (% of GDP) responded to the discovery in Senegal, measured in years since discovery and plotted against the non-HIPC peer average. Use the view toggle to switch between debt levels and change from discovery.

Borrowing Against Expectations

How public debt levels respond to giant petroleum discoveries. Central government debt as % of GDP, aligned to discovery year.

Source: IMF Global Debt Database 2.0 (1950–2024). Central government debt except Tanzania (general government). Amber shading indicates the first 5 years post-discovery. * = HIPC debt relief overlaps discovery window (shown dashed). Bold grey line = non-HIPC average.

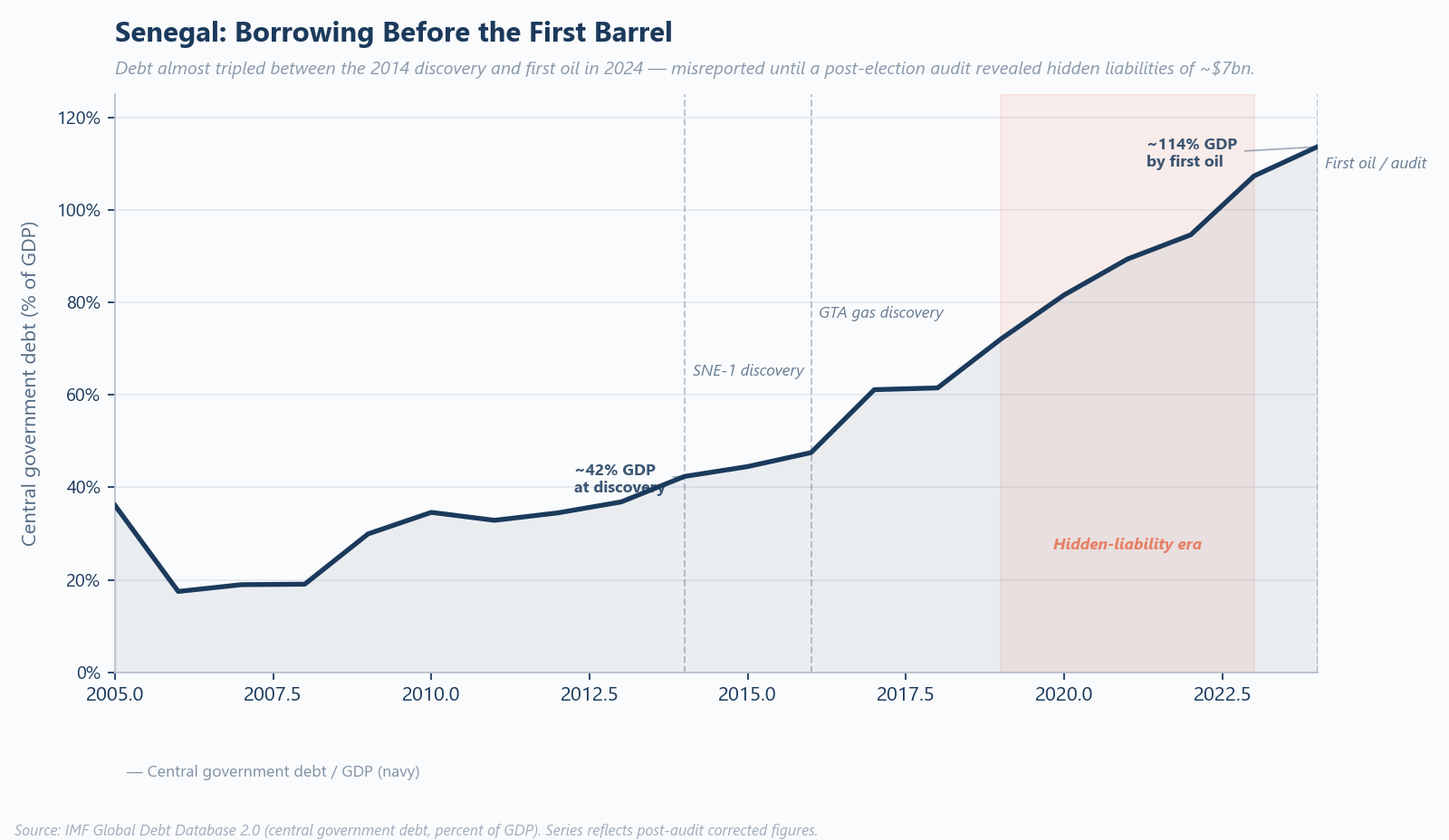

Borrowing Before the First Barrel

Central government debt as a share of GDP across Senegal's presource decade. Debt almost tripled between the 2014 SNE-1 oil discovery and first production in June 2024 — from around 42% of GDP to over 110% — with the sharpest rise coinciding with the 2019–2023 hidden-liability era that was only revealed after the post-election audit. Senegal entered the revenue phase already carrying the full weight of its presource borrowing.

Source: IMF Global Debt Database 2.0 (central government debt, percent of GDP). Series reflects post-audit corrected figures.

Lessons and Policy Implications

The presource curse can coexist with reasonable headline growth

Senegal's GDP growth averaged 5–6% during the presource decade. This was enough to mask the underlying fiscal deterioration. Countries and their international partners should look beyond headline growth to debt trajectories and fiscal transparency.

Election cycles and resource expectations are a toxic combination

Anticipated hydrocarbon revenues provided political licence for spending that was not yet fiscally grounded. The pattern — discovery → elevated expectations → election-cycle spending → debt accumulation — is the Ghana story with a ten-year fuse.

Off-balance-sheet liabilities are the new presource risk

Senegal's hidden debt came from state-owned enterprise liabilities, arrears, and PPP commitments excluded from official reporting. As governments navigate IMF debt limits, the risk migrates off-balance-sheet. Transparency frameworks must catch up.

Democratic institutions can correct — but not prevent — the presource curse

Senegal voted out the government responsible, ordered an audit, and exposed the hidden debt. But democratic correction after the fact does not undo debt accumulated before the election. Prevention remains the only effective remedy.

Entering the revenue phase with excessive debt eliminates the resource dividend

The cruelest outcome: oil revenues arrive to service debt taken on in anticipation of those same revenues. Senegal's Sangomar production exceeded targets in 2024 — but with debt above 120% of GDP, fiscal space to deploy those revenues is severely constrained.

References

- Cust, J. and Mihalyi, D. (2017). 'The Presource Curse'. Finance & Development, 54(4). IMF.

- IMF (2024). 'IMF Statement on Senegal'. Press release, October 2024.

- Senegal Court of Auditors (2025). Rapport sur l'Exécution des Lois de Finances 2019–2023.

- Woodside Energy (2024). Sangomar Phase 1 Operations Update.

James Cust · Development Economics · jamescust.com