African Eurobond issuers borrowed $111 billion in a decade. Five have defaulted. This note traces the mechanisms — from forecast-driven market access to maturity cliffs — that turn anticipated resource wealth into debt distress.

Between 2007 and 2024, twenty-one sub-Saharan African countries issued sovereign Eurobonds for the first time. Total issuance exceeded $111 billion at face value. The bonds carried coupons of 5-10 per cent, were denominated in US dollars, and typically had 10-year bullet maturities. Five of these twenty-one issuers have since defaulted or restructured: Seychelles (2008), Mozambique (2016), Zambia (2020), Ethiopia (2023), and Ghana (2022).

This is not a story of bad luck. It is a story of structural vulnerability — where optimistic growth forecasts enabled market access, commercial creditors replaced concessional lenders, and bullet maturity structures concentrated repayment risk into narrow windows.

The Mechanism: From Discovery to Distress

The over-borrowing cycle follows a consistent pattern. A major resource discovery or commodity price boom triggers upward forecast revisions. Credit rating agencies upgrade the sovereign. Investment banks pitch a debut Eurobond. The offering is massively oversubscribed — sometimes 5-8 times — which validates the narrative and opens the door to further issuance. The growth that justified the borrowing fails to materialise. Interest payments consume an increasing share of revenue. The country enters debt distress.

The note documents this cycle with data on all 21 SSA Eurobond issuers, tracking forecast errors at issuance vintage, coupon escalation across tranches, creditor composition shifts from concessional to commercial, and the interest burden trajectories that preceded each default.

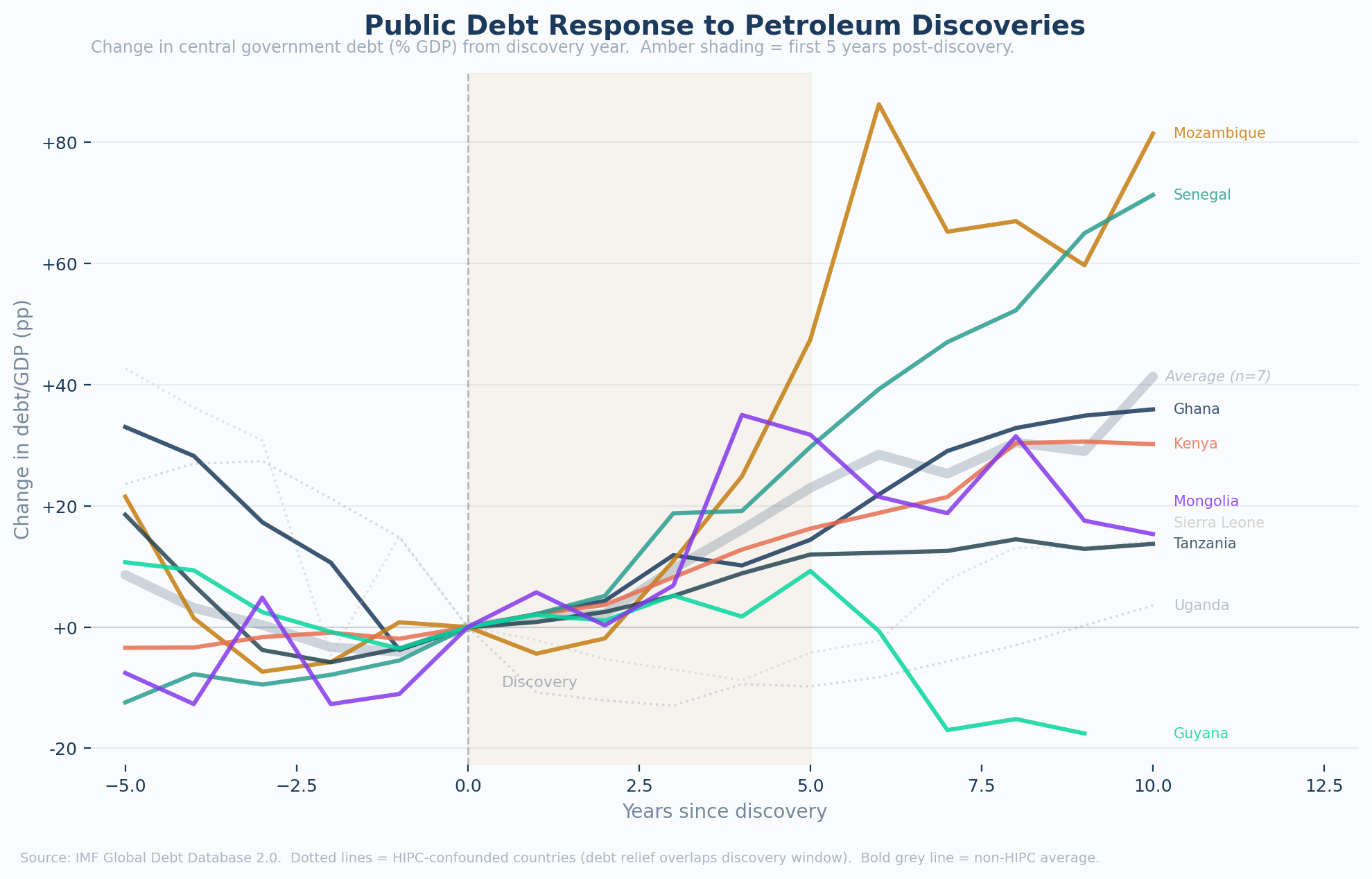

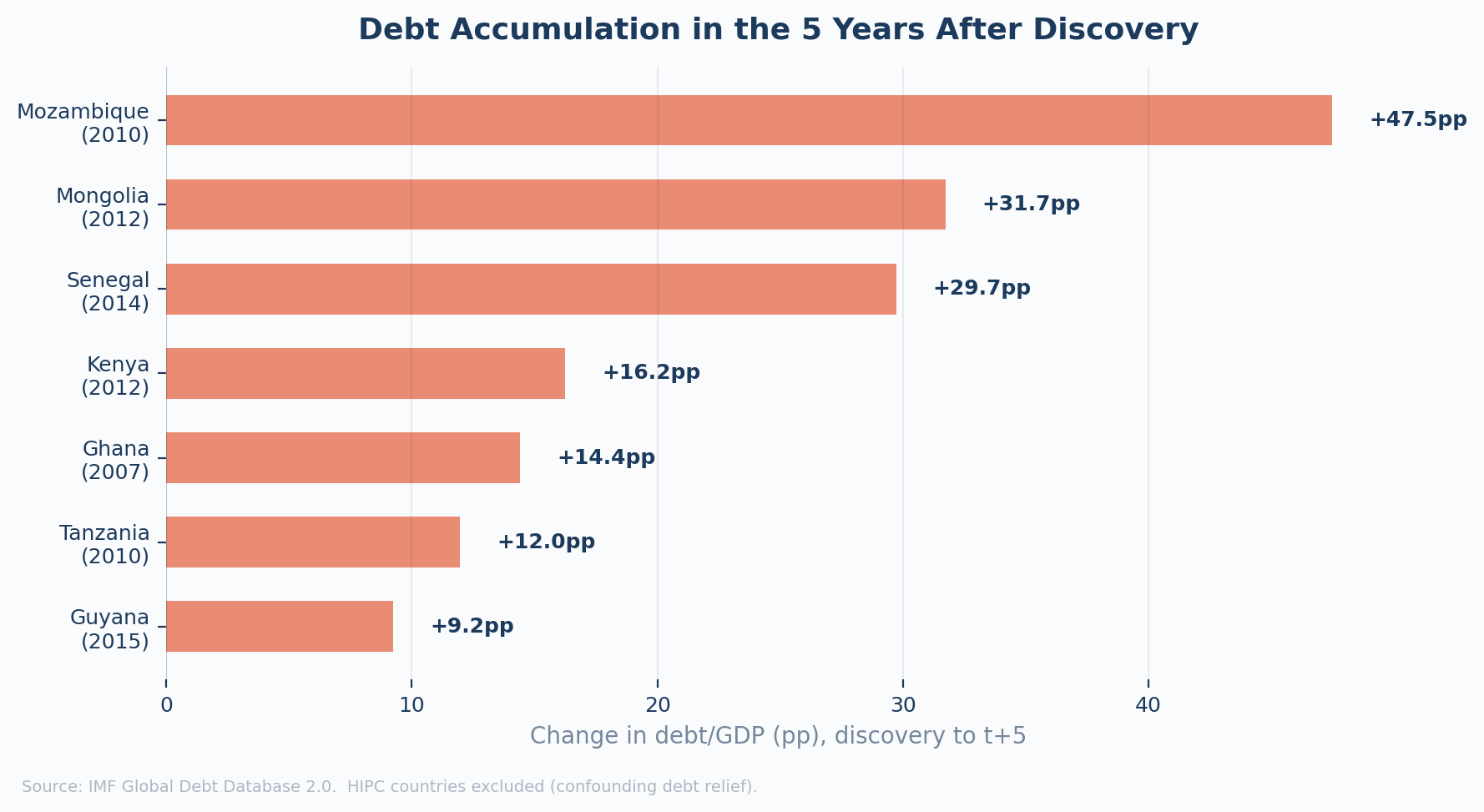

The Debt Response: Borrowing Begins at Discovery

The IMF Global Debt Database reveals a striking pattern: public debt levels rise sharply in the years immediately following giant petroleum discoveries — long before any revenue arrives. The chart below tracks central government debt as a share of GDP, aligned to discovery year. Among non-HIPC countries, the average debt accumulation is over 20 percentage points within a decade of discovery. Mozambique added 48 percentage points. Senegal added 30. Mongolia 32. Kenya 16. Ghana 14.

Key Findings

The evidence is stark across multiple dimensions. Forecast errors at the point of Eurobond issuance were large and systematic: Zambia's cumulative growth overestimate was 17.3 percentage points, Mozambique's 15.6 percentage points. Creditor composition shifted dramatically: the private share of SSA external debt rose from 22 per cent in 2006 to 42 per cent by 2023. Interest costs exploded: Ghana's interest payments consumed 47 per cent of government revenue at the point of default, up from 14 per cent at the time of its first Eurobond. And HIPC debt relief was systematically followed by commercial re-borrowing — Ghana was forgiven $6.5 billion, then borrowed $15.5 billion in Eurobonds at five times the interest rate.

Four Cases in Detail

Ghana

Oil · Discovery 2007 · Default 2022

From 31% of GDP at discovery to 87% at default. Borrowing accelerated even after Brent crashed in 2014 — a fiscal trajectory detached from the commodity cycle. Interest payments consumed 47% of revenue at the point of default.

Read full case studyMozambique

Gas · Discovery 2010 · Hidden debt 2016

Debt jumped from below 40% of GDP at discovery to above 90% within six years, driven by $2bn in hidden borrowings against gas revenues still a decade away. When the scandal broke, fourteen donors withdrew simultaneously.

Read full case studyZambia

Copper · HIPC relief 2005 · Default 2020

Received $6.5bn in HIPC relief in 2005, then borrowed its way back to default in fifteen years — the first African COVID-era sovereign default. Borrowing accelerated into the copper upswing and held on through the bust. Actual growth modestly beat IMF forecasts, yet debt ballooned anyway.

Read full case studySenegal

Oil & Gas · Discovery 2014 · IMF suspension 2024

A decade of systematic debt misreporting — $7bn in hidden liabilities. Public debt rose from 45% of GDP at discovery to over 100% by end-2023. When production finally began in June 2024, Senegal entered the revenue phase with the IMF programme suspended.

Read full case studyJames Cust · Development Economics · jamescust.com