In Brief

Zambia received $6.5 billion in HIPC debt relief in 2005 — a clean fiscal slate after two decades of copper-driven decline. Within fifteen years it had borrowed its way back to default, becoming the first African country to miss a sovereign Eurobond payment during the COVID era. The same commodity dependence, the same political economy of anticipated revenues, the same failure to save during the boom and diversify away from copper — the second time around.

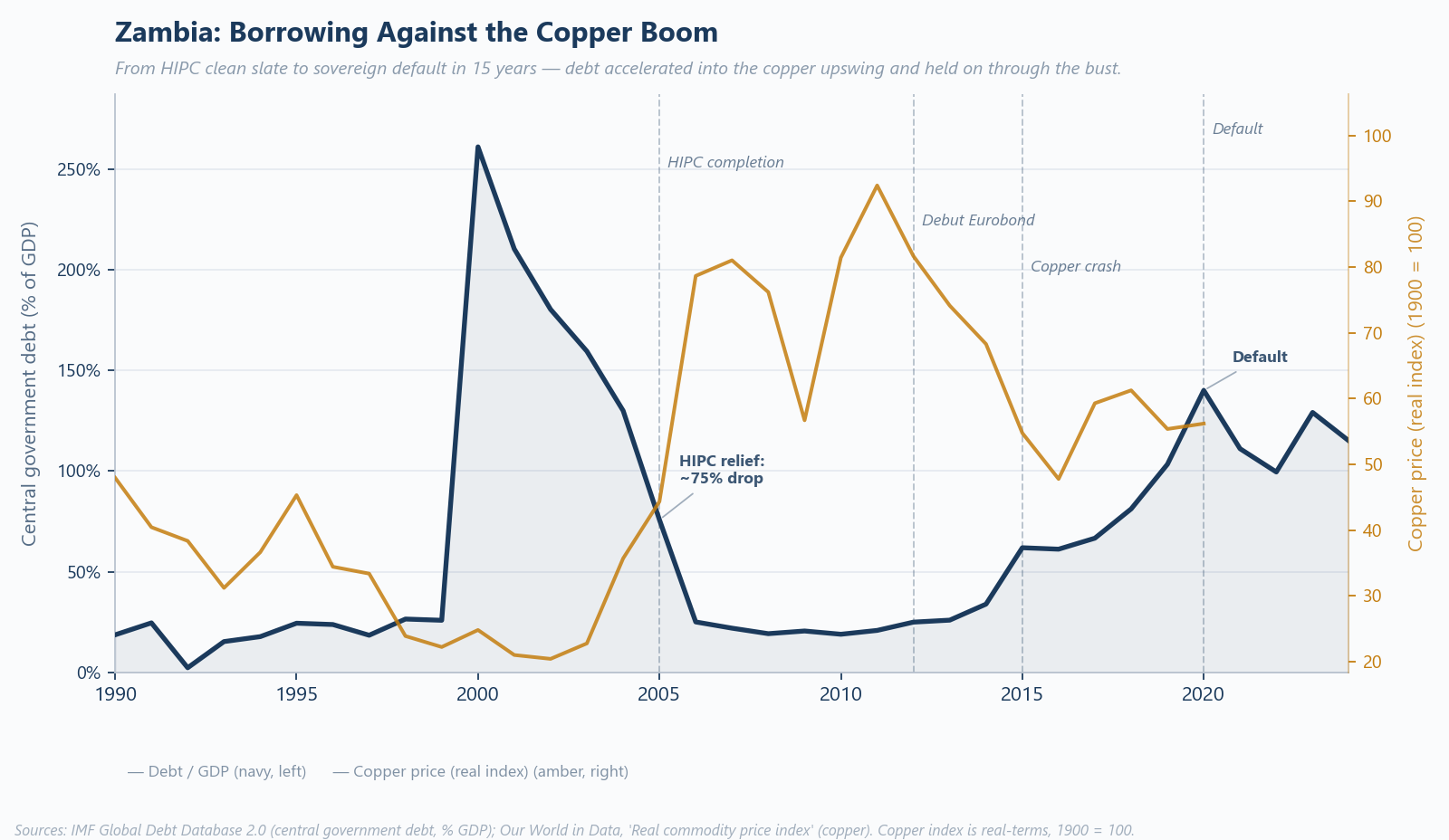

Borrowing Against the Copper Boom

Central government debt (navy, left) against the real copper price index (amber, right) across the post-HIPC cycle. The 2005 cliff drop shows $6.5bn of debt relief; the climb back to default in 2020 shows how quickly the second cycle played out. Debt accelerated into the copper upswing and held on through the bust.

Source: IMF Global Debt Database 2.0; Our World in Data real commodity price index (copper). Copper index is real terms, 1900 = 100.

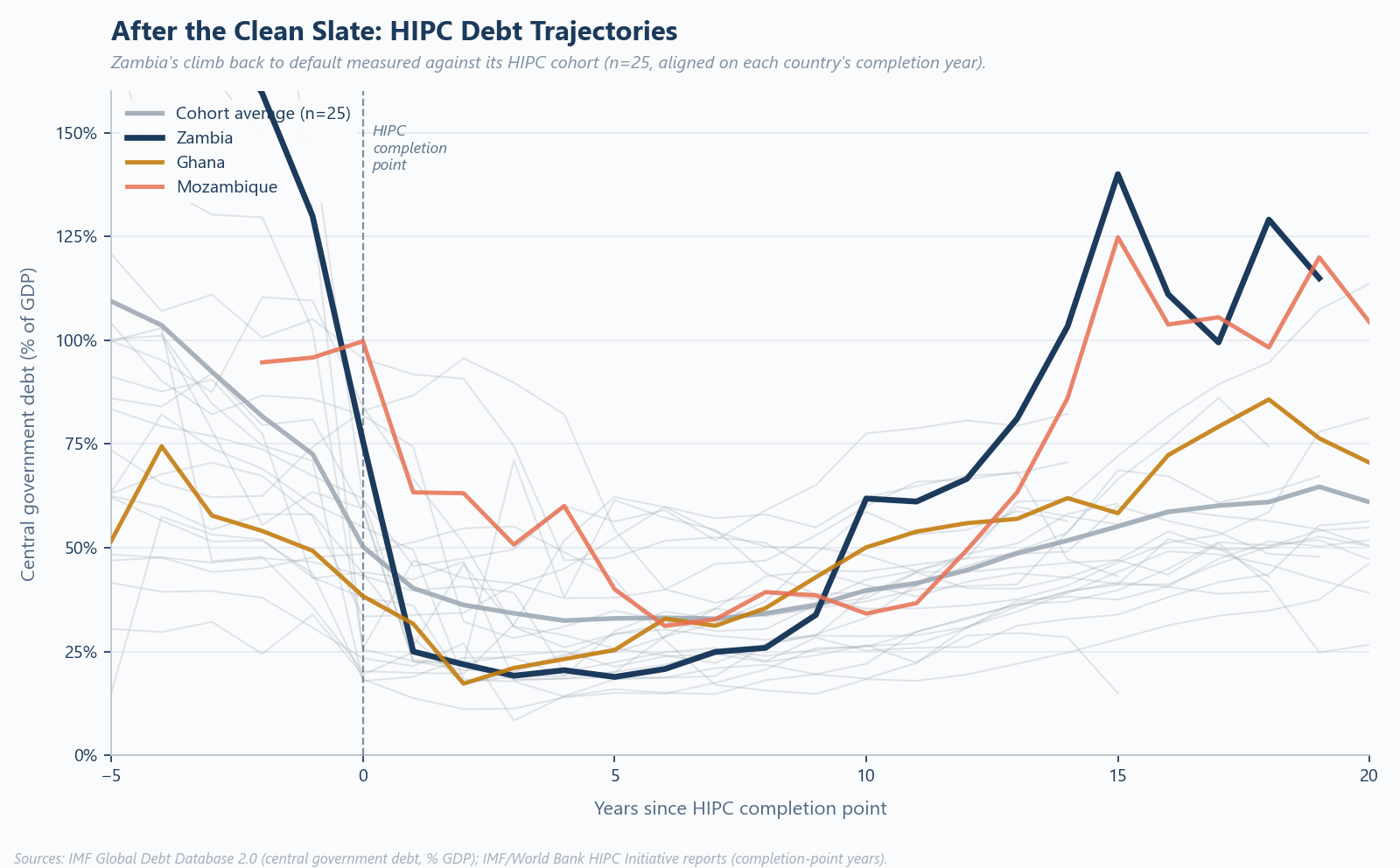

Zambia Against Its HIPC Cohort

Central government debt trajectories for 25 HIPC completion-point countries, each aligned on its own completion year (t=0). The cohort average (grey) settled near 30% of GDP at completion and climbed back to around 60% over two decades. Zambia (navy) climbed to above 140% within fifteen years — the fastest and steepest re-accumulation in the cohort. Ghana and Mozambique also outran the cohort average, but neither matched Zambia's trajectory.

Source: IMF Global Debt Database 2.0 (central government debt, % GDP); IMF/World Bank HIPC Initiative reports (completion-point years).

Lessons and Policy Implications

Debt relief is not a cure — it is a second chance

Zambia’s HIPC relief in 2005 reset the fiscal clock but did not change the underlying political economy of commodity dependence. The institutions, incentives, and structural vulnerabilities that produced the first resource curse were still in place when copper prices surged again. Without genuine structural transformation, a second cycle was probable.

Eurobond access is a warning sign, not a reward

When frontier markets gain access to commercial borrowing at low spreads during commodity booms, the rational policy response is caution, not acceleration. The favourable terms on Zambia’s 2012 debut Eurobond reflected the commodity cycle and a global search for yield — not a permanent improvement in creditworthiness. Borrowing heavily at the top of the cycle is the defining error of the Zambian case.

Chinese infrastructure lending requires the same scrutiny as commercial debt

Zambia’s opaque borrowing from Chinese state lenders — for road, power, and other infrastructure — added substantially to the debt burden while falling outside the Eurobond framework that investors monitored. The complexity this introduced to the eventual restructuring extended the period of debt distress and imposed real costs on the Zambian economy.

The G20 Common Framework is too slow for the countries it is meant to help

Zambia’s restructuring took over three years from default to agreement, during which debt service consumed fiscal space needed for recovery and development investment. The architecture for sovereign debt restructuring is inadequate for a world of Eurobond holders, Chinese state lenders, and multilateral creditors with divergent interests.

Commodity diversification cannot wait for the boom to end

The window to invest windfall revenues in economic diversification is during the boom — when fiscal space exists and political legitimacy to undertake structural reform is greatest. By the time copper prices fell in 2015, Zambia’s fiscal space had already been consumed by debt service and committed expenditure.

References

- Cust, J. and Mihalyi, D. (2017). 'The Presource Curse'. Finance & Development, 54(4), December. Washington DC: IMF.

- Cust, J. and Mihalyi, D. (2017). 'Evidence for a Presource Curse? Oil Discoveries, Elevated Expectations, and Growth Disappointments'. World Bank Policy Research Working Paper 8140. Washington DC: World Bank.

- IMF (2020). Zambia: Request for Emergency Financing under the Rapid Credit Facility. IMF Country Report No. 20/242. Washington DC: IMF.

- IMF (2023). Zambia: Fifth Review under the Extended Credit Facility Arrangement. IMF Country Report No. 23/165. Washington DC: IMF.

- Jubilee Debt Campaign (2020). Zambia's Debt Crisis: How Did We Get Here? London: Jubilee Debt Campaign.

- Ruzzante, M. and Sobrinho, N. (2022). 'The Fiscal Presource Curse: Giant Discoveries and Debt Sustainability'. IMF Working Paper 22/10. Washington DC: IMF.

- World Bank (2022). Zambia Economic Brief: Managing Debt for Recovery and Resilience. Washington DC: World Bank.

James Cust · Development Economics · jamescust.com